A balance sheet shows what a business owns, and what it owes. When a lender approves you for a loan, they are taking on risk—the risk of whether the loan will be repaid. How risky is your business? Your balance sheet is part of the answer.

In a single document, a balance summarizes all of a business’s assets and liabilities for a certain period of time. “Assets and liabilities” are financial terms for the money or valuable property you have access to, and the money you owe now or may owe in the near future.

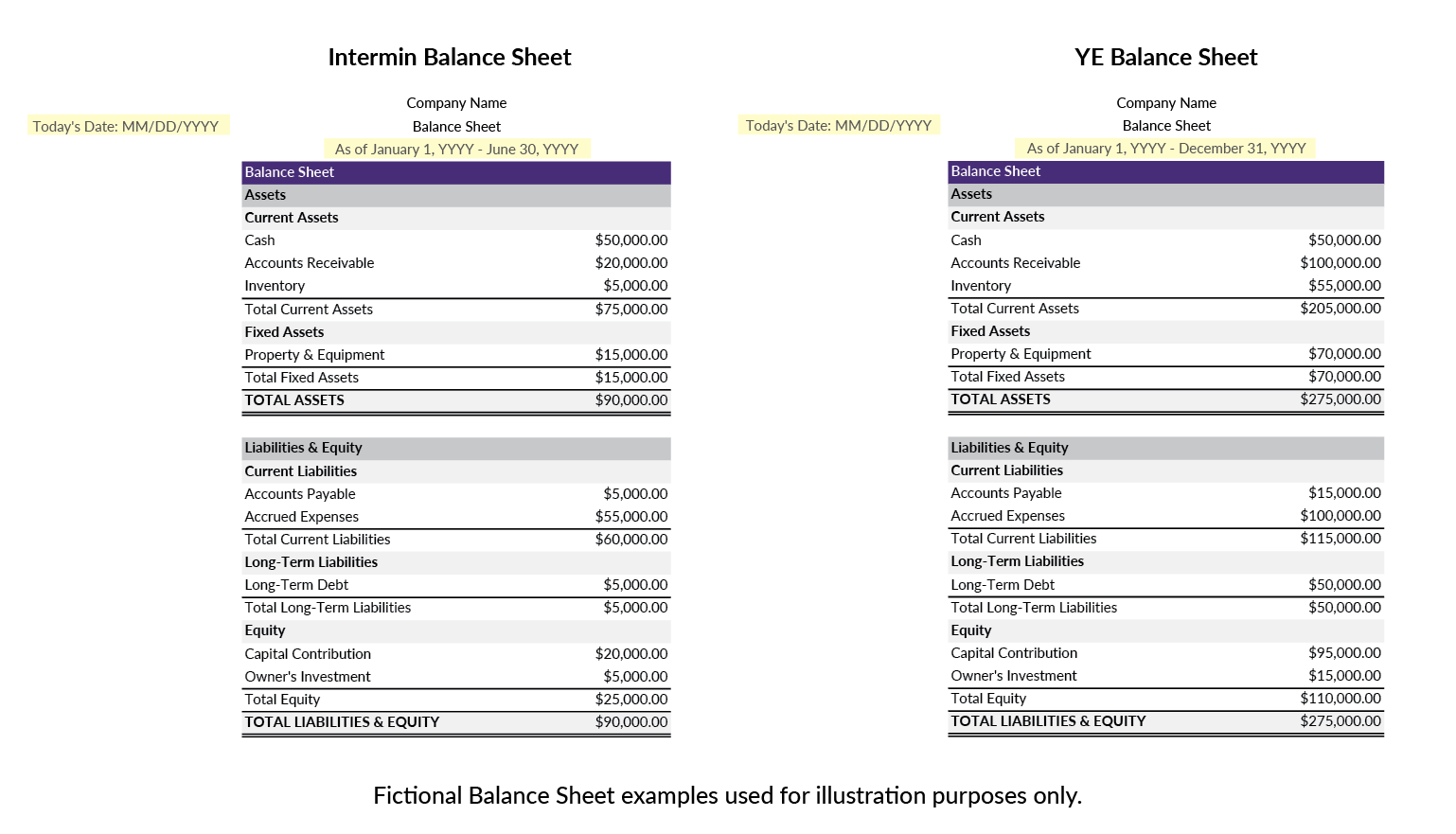

Why are Balance Sheets Important?

A balance sheet provides important information that lenders need to make a decision about a loan. Because it summarizes your assets and debts, the balance sheet shows if you have personal funds and/or resources that could be used to pay back your business loan if your other sources of revenue are not enough. The SBA requires them when applying for an SBA 7(a) loan, and other lenders do as well. The lender will also ask for updated balance sheets during your repayment period.

Small business lenders and investors use balance sheets to make calculations that they need to assess a business, like its debt-to-income ratio.

For business owners and company managers, preparing and reviewing these statements, and noting changes, gives important insight into the business. Over time, financial statements show trends and opportunities for improvement in simple black and white.

What information is shown on a Balance Sheet?

Assets:

- Cash

- Accounts receivable

- Inventory

- Property

Liabilities:

- Rent

- Wages

- Utilities

- Taxes

- Loans

- Shareholders’ equity, if you have investors

Statement Timeframes

Other financial statements like Profit & Loss show what transactions occurred within a set period of time:

- Year-end (YE) statement: Covers a whole fiscal or calendar year

- Interim statement: Covers a shorter period of time, typically a quarter or six months

Balance sheets, however, capture a particular moment. “These are our assets and liabilities on this date.”

Common Mistakes to Avoid on Profit & Loss (P&L) Statements

- The wrong date in the wrong place. The dates on this statement are very important and are often not entered correctly when they’re not prepared by a finance professional. The statement has to show the time period the statement refers to, whether it’s year-end or interim, and it also must include the date when the statement was prepared.

- Omitting transactions or recording them incorrectly. The most common mistake on a balance sheet, especially when prepared by a business owner instead of a professional bookkeeper or accountant, is missing items like petty cash, supplies or other expenses, inputting numbers wrong.

- Forgetting to update inventory. If you don’t tally up current inventory before preparing a balance sheet, the assets will not be accurate.

- Inconsistent accounting – cash versus accrual. Accounting documents show your income and expenses either on a cash basis (money received/paid) or on an accrual basis (money invoiced/owed, but not necessarily paid yet). These documents include your tax returns! It’s important to make sure all your financial documents use one or the other consistently, and triple check your tax returns to make sure they match.

Preparing balance sheet correctly avoids questions and revisions that can slow down the process when applying for a small business loan or purchasing commercial real estate. If you are not confident in your ability to prepare and update your balance sheet, consider hiring an accountant or CPA to put your business’s best foot forward.